Quick Answer

EV battery prices are falling around the world, but the decline is not happening evenly across China, North America, Europe, and stationary storage markets. EV battery prices are falling because raw material costs have cooled from their 2022 highs, LFP batteries are spreading quickly, manufacturing scale keeps improving, and China has built far more battery production capacity than the market can easily absorb.

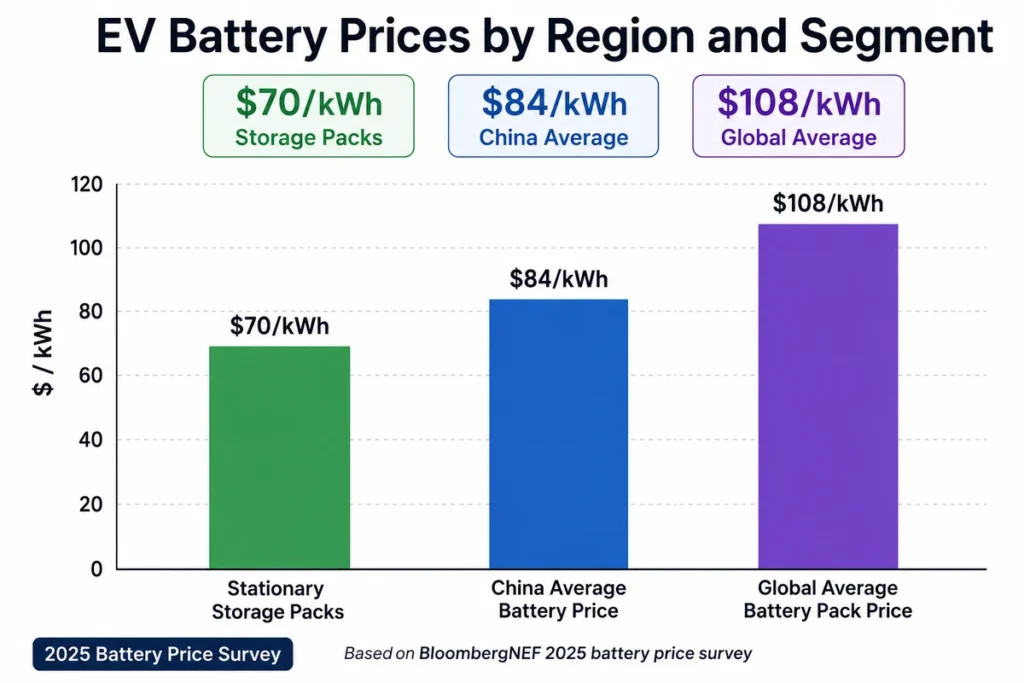

But the price drop is not happening equally everywhere. China now has the world’s lowest battery prices because it combines massive manufacturing scale, intense supplier competition, strong LFP adoption, local supply chains, and in some cases overcapacity. According to BloombergNEF, average lithium-ion battery pack prices fell to $108/kWh in 2025, while average battery prices in China dropped to $84/kWh. Stationary storage packs fell even further, reaching about $70/kWh in 2025, according to BloombergNEF’s battery price survey.

The important point for EV buyers is this: lower battery prices should help make EVs cheaper over time, but the benefit will depend on where the vehicle is built, which battery chemistry it uses, how much local manufacturing is required, and how much of the cost reduction automakers pass on to consumers.

Introduction: Battery Prices Are Falling, But the Story Is Getting More Complicated

For years, the EV industry has treated falling battery prices as one of the biggest reasons electric vehicles would eventually become cheaper than gasoline cars. That basic idea is still true. The battery pack remains one of the most expensive parts of an EV, so every dollar saved per kilowatt-hour matters. But the battery cost story is no longer as simple as “battery prices are falling, so all EVs will get cheaper.”

In 2025 and 2026, the market became more uneven. China moved faster than almost everyone else. LFP batteries became more dominant in affordable EVs and stationary energy storage. Battery storage demand surged. Raw material prices fell, then began showing signs of volatility again. At the same time, the United States and Europe pushed harder for local battery supply chains, which can improve security but often raises near-term production costs.

That is why two EVs with similar battery sizes can have very different cost structures depending on where their cells are made, what chemistry they use, and how mature the supply chain is.

EV Insight Daily has already covered the broader trend in EV Battery Prices 2026: Why Costs Keep Falling. This article goes one level deeper. Instead of only asking why battery prices are falling, we need to ask why they are falling faster in some places than others.

Why EV Battery Prices Are Falling Globally

BloombergNEF reported that average lithium-ion battery pack prices fell to $108/kWh in 2025, even though some metal prices were rising again by the time the survey was released. That number matters because it shows how far the industry has come from the early EV era, when battery packs cost several hundred dollars per kilowatt-hour.

A lower average pack price helps automakers in several ways. It can reduce the cost of building an EV. It can allow a larger battery at the same vehicle price. It can help make entry-level EVs more competitive. It can also improve the economics of battery storage systems that support the electric grid.

But averages can hide a lot. A global average battery price combines very different products: EV packs, bus batteries, commercial vehicle batteries, and stationary storage packs. It also blends very different regions. A pack built in China using LFP cells from a highly scaled supplier does not have the same cost structure as a pack built in North America using locally sourced materials, lower-volume production, and different regulatory requirements. That is where the real story begins.

China’s Battery Prices Are in a Different League

China’s battery cost advantage is not new, but it became even more visible in 2025. BloombergNEF reported that average battery prices in China fell to $84/kWh in 2025, helped by lower input costs, overcapacity, aggressive price competition, and strong preference for LFP cells. The International Energy Agency also noted that regional battery price disparities widened, with China’s pack prices significantly below those in North America and Europe in 2025, according to the IEA Global EV Outlook 2026 battery section.

This is not just about cheap labor. That explanation is too simple and misses what has actually happened. China has built an enormous battery ecosystem. Cell manufacturers, cathode producers, anode suppliers, electrolyte companies, separator makers, pack integrators, EV brands, and energy storage developers operate close to each other. When production volumes rise, suppliers learn faster. When factories are highly utilized, fixed costs are spread over more cells. When many companies compete for the same contracts, margins get squeezed.

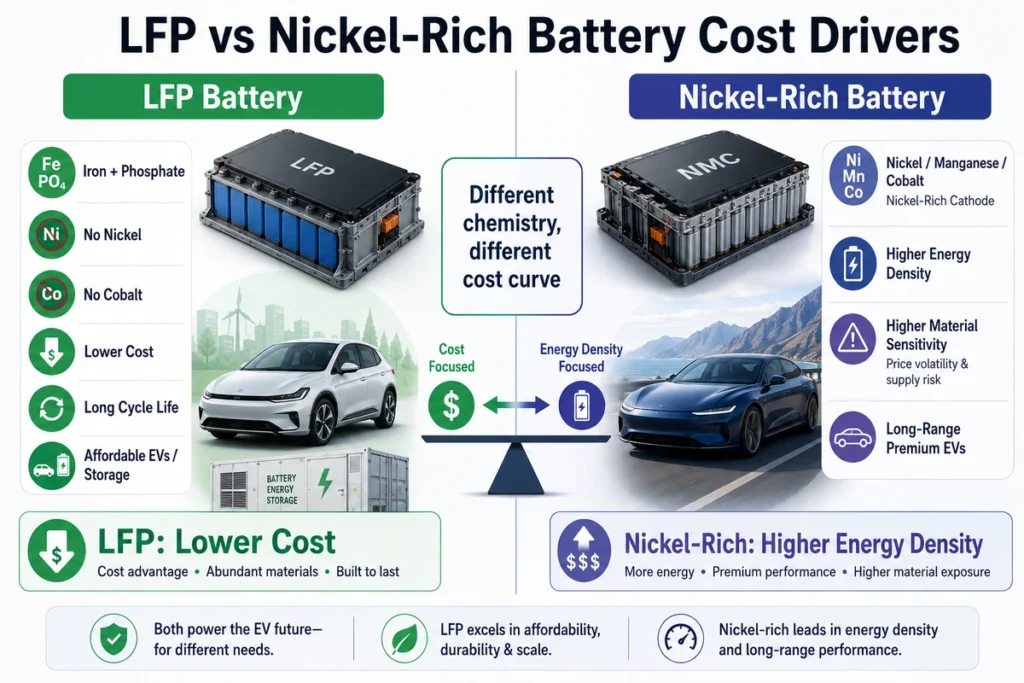

That is painful for weaker suppliers, but it lowers prices for buyers. China also has a major advantage in LFP. For many years, Western automakers leaned more heavily on nickel-based chemistries such as NMC and NCA because they offered higher energy density. Chinese companies, by contrast, kept improving LFP and scaled it aggressively. That decision now looks very important.

As discussed in LFP vs NMC Batteries: Which EV Battery Is Better in 2026?, LFP does not need nickel or cobalt in the cathode. That makes it less exposed to some of the most expensive and volatile battery metals. It also fits well with standard-range EVs, electric buses, entry-level vehicles, and grid storage systems where cost and durability matter more than maximum range.

Overcapacity Is Pushing Prices Down

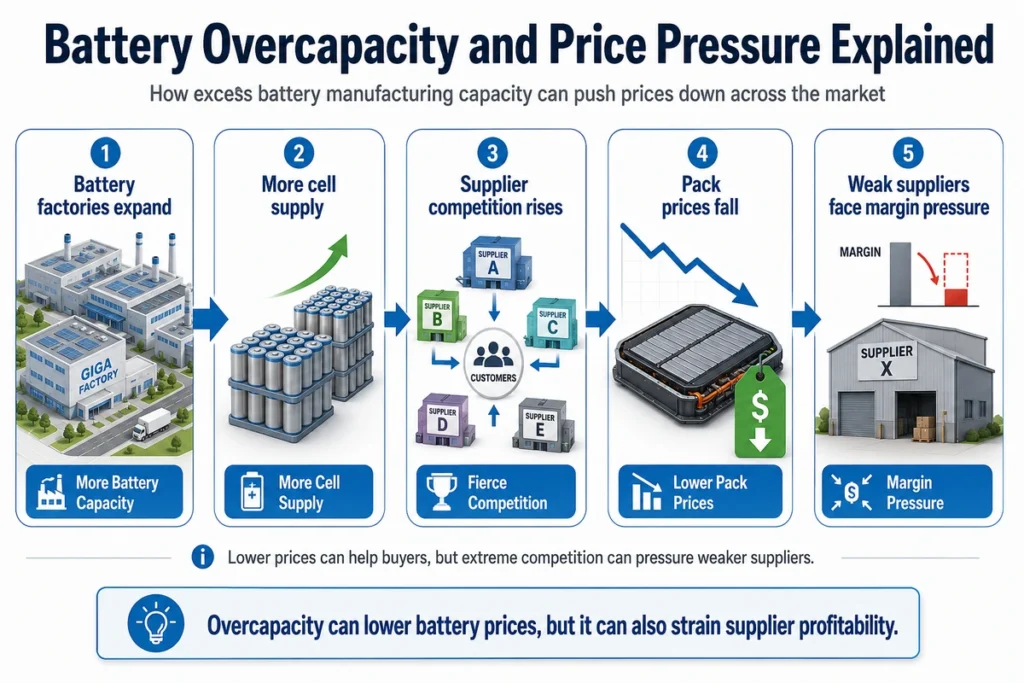

One reason battery prices fell so sharply in China is that the industry built capacity faster than demand could comfortably absorb. Overcapacity sounds like an abstract economic term, but the effect is easy to understand. If many battery factories can produce more cells than customers currently need, suppliers fight harder to win orders. That can push prices down quickly.

China’s own government has recognized this risk. Reuters reported in early 2026 that China’s industry ministry urged battery manufacturers to optimize capacity and reduce overcapacity risks in the EV and energy storage battery sectors. The article noted concerns about market competition and the need for better supervision within the battery industry, according to Reuters.

For EV buyers, overcapacity can look like good news because it lowers battery costs. For battery manufacturers, it is more complicated. Falling prices can reduce margins, delay new projects, and force consolidation. Smaller or less efficient companies may struggle. Stronger companies with better technology, scale, and vertical integration may gain more market share.

This is one reason BYD and CATL are so important. They are not just battery suppliers. They sit near the center of a huge industrial system that can move quickly, cut costs, and push technology into mass production.

LFP Is Changing the Cost Curve

Battery chemistry is one of the biggest reasons battery prices are falling unevenly. LFP batteries are generally cheaper than nickel-rich chemistries because they avoid nickel and cobalt. They also have good cycle life and strong thermal stability. Their main disadvantage is lower energy density, although pack-level engineering has reduced that gap in many real-world vehicles.

For a long-range luxury SUV, an automaker may still prefer a nickel-rich chemistry because range, weight, and performance matter. But for a standard-range sedan, city EV, commercial fleet vehicle, or energy storage system, LFP can be the better economic choice.

That is why LFP is no longer just a “cheap EV battery.” It is becoming a mainstream chemistry for large parts of the market. EV Insight Daily covered this broader shift in Why There Will Not Be One Winning EV Battery Chemistry. The battery market is not moving toward one universal chemistry. It is splitting by use case.

This matters for prices because regions that use more LFP can see faster cost declines. China has the strongest LFP supply chain, so its vehicles and storage systems can benefit sooner. The U.S. and Europe are also moving toward LFP, but they are still building local supply chains and qualifying suppliers. The result is a timing gap. The chemistry may be cheaper in theory, but the full cost benefit depends on scale, sourcing, production yield, logistics, and policy.

Stationary Storage Is Now the Lowest-Cost Segment

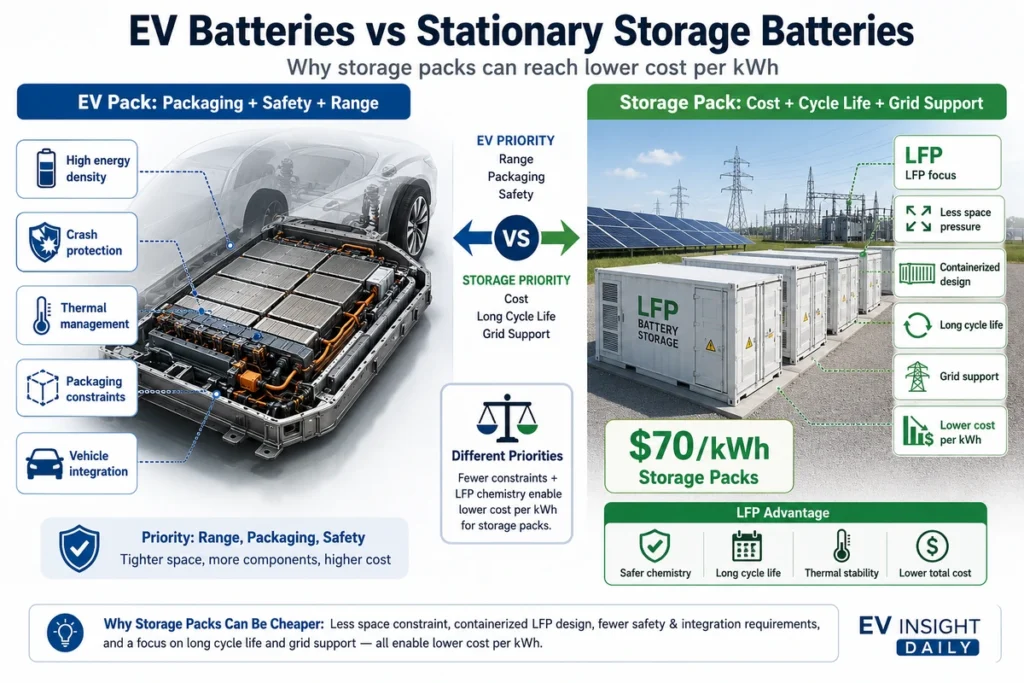

One of the most interesting details from BloombergNEF’s 2025 survey is that stationary storage packs fell to about $70/kWh, making storage the lowest-priced battery segment for the first time. That is a major shift.

For years, EVs were the main driver of battery scale. Electric cars demanded huge volumes of cells, and battery makers optimized around automotive requirements. But grid storage has become large enough to shape the battery market on its own.

Stationary storage does not need the same energy density as a passenger EV. A battery container sitting next to a solar farm does not care about vehicle range, acceleration, or cabin space. It cares about cost, safety, cycle life, reliability, and the ability to charge and discharge repeatedly over many years.

That makes LFP a natural fit. This trend connects directly with the growth of grid-scale battery systems, AI data center power demand, and renewable energy integration. EV Insight Daily recently covered this in Why EV Battery Companies Are Betting Big on Grid Energy Storage and AI Data Center Battery Storage: 5 Reasons Demand Is Rising.

The important takeaway is that EV battery prices and grid storage prices are now linked. When storage demand rises, it can support larger LFP production volumes. Larger LFP volumes can lower costs. Lower costs can make both storage projects and affordable EVs more attractive.

But there is also a downside. If storage demand becomes extremely strong, it can compete with EVs for cells, lithium, manufacturing capacity, and supply-chain attention. Battery prices do not fall in a straight line forever.

Raw Material Prices Still Matter

Battery prices are not only about factory scale. They are also tied to raw materials. Lithium, nickel, cobalt, graphite, manganese, copper, and other materials can move sharply in price. In 2022, high lithium prices became a major concern for EV affordability. Later, lithium prices fell significantly as supply expanded and demand growth cooled in some markets. That helped battery prices decline.

Goldman Sachs previously argued that falling raw material costs would be a major reason EV battery prices could fall sharply, with its researchers projecting battery prices could move toward $80/kWh by 2026 in an October 2024 analysis from Goldman Sachs.

But raw material relief is not guaranteed forever. The IEA’s Global Critical Minerals Outlook 2025 points out that demand for key energy minerals continued to grow strongly in 2024, with lithium demand rising nearly 30%. That tells us something important: even when battery prices fall, the underlying mineral system remains under pressure.

Reuters also reported in July 2026 that battery metals were recovering from the lows of 2024–2025, with policy actions, export controls, and supply restraints affecting lithium, nickel, and cobalt markets. The same Reuters analysis noted that grid-scale storage has become a larger demand driver, especially in China, and that storage mostly uses LFP batteries, which do not rely on nickel or cobalt in the same way as nickel-rich EV chemistries.

So yes, raw material prices helped push battery prices down. But future price volatility can still affect the market. This is especially true for regions trying to build local supply chains while competing against China’s mature and highly scaled ecosystem.

Why U.S. and European Battery Prices Are Higher

If battery technology is improving everywhere, why are batteries still more expensive in the United States and Europe? The first reason is scale. China has more battery manufacturing volume, more suppliers, and more domestic demand for affordable EVs and storage systems. The U.S. and Europe are expanding, but many plants are newer, smaller, or still ramping up.

The second reason is localization. Local battery production can reduce geopolitical risk and qualify vehicles for incentives, but it can also raise near-term costs. New factories need time to reach high yield. Local material processing may be more expensive. Labor, permitting, energy, financing, and environmental compliance costs can differ by region.

The third reason is chemistry mix. North America historically leaned more heavily on nickel-based chemistries, especially for long-range EVs. That made sense when consumers expected 300-plus miles of range and automakers wanted to compete with gasoline vehicles on long-distance driving. But nickel-rich packs are usually more expensive than LFP packs.

The fourth reason is policy. Tariffs, local-content rules, tax credits, and trade restrictions can change the effective cost of batteries. A cheaper imported cell may not be the cheapest option after tariffs or incentive rules are considered. A locally made cell may cost more at the factory gate but help the vehicle qualify for consumer incentives. This is why “battery cost” is not always the same as “vehicle price.” Automakers make decisions based on total economics, not just the lowest cell price.

Lower Battery Prices Do Not Automatically Mean Cheaper EVs

A common mistake is assuming that lower battery prices immediately show up as lower sticker prices. Sometimes they do. More affordable LFP-based EVs in China are a good example. When battery costs fall and competition is intense, automakers often pass savings to buyers because they need to defend market share.

But in other markets, savings may be absorbed elsewhere. Automakers may use lower battery costs to improve margins, add more range, include better thermal management, upgrade software and electronics, or offset higher labor and compliance costs. Dealers, tariffs, logistics, and local incentive changes can also affect final pricing.

There is also the issue of vehicle segment. Battery cost reductions help most when automakers are trying to build lower-cost EVs. A $3,000 battery cost reduction can be huge for a $25,000 compact EV. It matters less for an $85,000 luxury EV where brand, performance, software, interior, and margins play a larger role. That is why U.S. buyers may not feel the full battery price decline right away. The global trend is positive, but the local market can lag.

What This Means for EV Buyers

For EV shoppers, falling battery prices are still good news. They should gradually improve affordability, increase model variety, and reduce the fear that EV batteries are exotic, fragile, or impossible to replace.

But the benefit will not arrive evenly. Affordable EVs using LFP batteries are likely to see the clearest cost improvements. Standard-range models may become more attractive because LFP gives automakers a way to lower cost without sacrificing durability. Longer-range premium vehicles may still use nickel-rich chemistries where energy density matters more.

Used EV buyers may also benefit. As new battery prices fall, the long-term replacement-cost fear becomes less severe. That does not mean battery replacement is cheap today, but it does mean the direction is improving. For more on battery longevity and used EV confidence, see How Long Do EV Batteries Last? Real-World Data 2026.

The bigger change may be psychological. For years, EV batteries were seen as expensive and uncertain. Now the market is learning that battery costs can fall, chemistries can diversify, and packs can be designed for different use cases. That does not remove every concern. It just makes the EV battery market look more like a maturing industry.

The Risk: Prices Can Fall Too Fast

Falling prices sound good, but extreme price competition can create risks. If battery prices fall because of better technology and scale, that is healthy. If they fall because too many suppliers are selling below sustainable margins, the market can become unstable. Weak companies may collapse. Projects may be delayed. Quality can become a concern if suppliers cut corners. Governments may step in to control capacity expansion.

That is why China’s overcapacity issue matters globally. Cheap batteries can accelerate EV adoption and grid storage deployment, but a disorderly market can also create volatility. Automakers and energy storage developers need low prices, but they also need reliable suppliers that will still exist years later to support warranties, service, and future production. For consumers, the best outcome is not simply the lowest possible battery price. It is a stable battery industry that can produce safe, durable, affordable packs at scale.

Conclusion: Battery Prices Are Falling, But Geography Matters

EV battery prices are falling, but the decline is uneven. China has the lowest prices because it combines scale, LFP leadership, local supply chains, intense competition, and overcapacity. The U.S. and Europe are improving, but they face higher costs as they build local battery ecosystems and reduce dependence on imported cells and materials.

LFP is one of the biggest reasons prices are falling. It reduces reliance on nickel and cobalt, works well for affordable EVs, and is becoming the dominant chemistry for stationary storage. Raw material prices have also helped, although lithium and other battery metals remain volatile.

For EV buyers, the message is encouraging but not simple. Battery prices are moving in the right direction, but not every vehicle, region, or chemistry will benefit at the same speed. The next phase of EV affordability will depend not only on better batteries, but also on where those batteries are built, which chemistry they use, and whether automakers pass the savings on to consumers.

FAQs

Why are EV battery prices falling?

EV battery prices are falling because of larger manufacturing scale, lower raw material costs compared with the 2022 peak, rising LFP adoption, improved production efficiency, and intense competition among battery suppliers.

Why are batteries cheaper in China?

China has lower battery prices because it has the world’s largest battery manufacturing ecosystem, strong LFP supply chains, high production volume, intense supplier competition, and in some cases overcapacity. These factors push prices lower than in North America and Europe.

What is the cheapest EV battery chemistry?

LFP is generally one of the lowest-cost mainstream EV battery chemistries because it avoids nickel and cobalt. It is especially attractive for standard-range EVs, entry-level models, electric buses, commercial vehicles, and stationary storage.

Does a lower battery price mean EVs will become cheaper?

Usually, yes over the long term, but not always immediately. Automakers may use battery savings to reduce prices, increase range, improve margins, or offset other costs. Local incentives, tariffs, labor costs, and supply-chain rules also affect the final vehicle price.

Why are stationary storage batteries so cheap?

Stationary storage batteries do not need the same energy density as EV batteries. They can prioritize cost, safety, cycle life, and reliability. That makes LFP a strong fit, especially for grid-scale storage systems.

Could battery prices rise again?

Yes. Battery prices can rise if lithium, nickel, graphite, copper, or other material prices increase sharply. Policy changes, export controls, supply disruptions, and strong demand from EVs and grid storage can also affect prices.